Mortgage Savings Calculator

- Adding extra payments, whether monthly, yearly or both, can alter your loan’s scheduled payoff timeline.

- How much interest can you save?

- How many years can you shave off your loan term?

- What’s the total amount you’ve contributed in extra payments over time?

- Take a look!

| Date | Payment | Principal | Interest | Extra Payment | Remaining Balance |

|---|

How Amortization Works

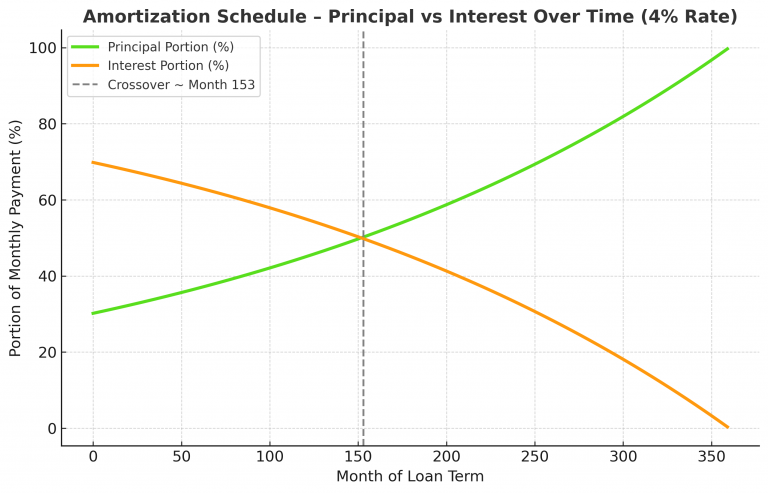

Amortization is the process of paying off a loan through regular, fixed monthly payments over a set period of time. With a mortgage, your payment each month stays the same, but the way it is applied shifts over time between interest and principal. At the very beginning, the outstanding balance is at its highest, so most of your payment goes toward interest, which is the lender’s charge for borrowing the money. Only a small portion is applied to reducing the principal balance. As each month passes and the balance slowly decreases, the amount of interest due also drops. This allows more and more of your payment to go toward principal, even though the total payment amount never changes. By the later years of the loan, the majority of your monthly payment is applied directly to paying down the balance, with only a small fraction going to interest. The crossover where the portion of the interest payment equals the portion of the principal payment is approximately 12 years and 9 months on a 30 year fixed loan.

How Extra Payments At The Beginning Affect Interest Savings

When you make extra payments at the beginning of a mortgage, those payments go straight toward reducing the principal balance. Because interest is always calculated on the remaining balance, lowering that balance early has a compounding effect. Each month that follows, the interest owed is slightly less, which means a bigger portion of your regular payment is applied to principal instead of interest. This cycle accelerates the payoff schedule because every extra dollar today reduces the interest charged tomorrow.

The reason this is so powerful at the beginning of the loan is that interest costs are front-loaded in the amortization schedule. In the first few years, the majority of each payment is interest, and only a small fraction chips away at principal. By making extra payments during this period, you are directly attacking the balance at a time when the lender is charging the most interest. This can lead to tens of thousands of dollars in savings and shave years off the loan, compared to making the same extra payments much later when most of the payment is already going to principal.

To calculate mortgage payments:

Input Loan amount, interest rate and loan term in years, Select the calculate button. results end up under monthly housing payments.

To calculate savings with extra payments:

Input extra monthly payments or extra yearly payments, or both. Select the calculate button. Savings results are at the bottom. Select a start date, then select the amortization button if to see the extra payments being applied through out the life of the loan.

Pay Schedule: This number is will decrease as more extra payments are applied towards the interest.

Years Saved: The amount of years and months taken off the payoff schedule based on extra payments.

Interest Saved: Interest amount saved taken from total interest paid when extra payments are calculated.

Extra Payments Made: The total of all the extra payments made to achieve interest saved.